Fixed Annuity Income Rider

What is a Fixed Annuity Income Rider?

It would be great if your bank offered you an account that:

It would be great if your bank offered you an account that:

• Paid you a competitive interest rate.

• Provided a guaranteed lifetime of income even if your balance dropped to zero.

• And gave you access to your cash in case of an emergency.

Unfortunately, banks do not offer an account like this. However, insurance companies offer a fixed annuity with an income rider feature. An annuity income rider added to a deferred fixed annuity can provide you a future lifetime of income you cannot outlive.

Why a Deferred Fixed Annuity?

Think of a deferred fixed annuity like a savings account in the bank. They are both savings vehicles, they both pay interest, but that’s where the similarities end. A deferred fixed annuity (an annuity with a minimum interest rate) typically offers an interest rate guarantee period that is good for one year at a time but is less liquid than a bank account. In a deferred fixed annuity your principal is protected and interest earned is tax-deferred (taxes postponed) until the earnings are taken out.

What this means is

A deferred fixed annuity is a savings vehicle from an insurance company that provides a safe haven for your money. You can buy it with a lump sum payment or with installment payments. Most fixed annuities are designed to pay you a competitive rate of return good for one year at a time. Also, the annuity renewal rate is competitive with prevailing interest rates of other similar products at the time. However, the annuity renewal rate can be no less than the contractually guaranteed minimum renewal rate after the first year.

is a savings vehicle from an insurance company that provides a safe haven for your money. You can buy it with a lump sum payment or with installment payments. Most fixed annuities are designed to pay you a competitive rate of return good for one year at a time. Also, the annuity renewal rate is competitive with prevailing interest rates of other similar products at the time. However, the annuity renewal rate can be no less than the contractually guaranteed minimum renewal rate after the first year.

Your income three (3) ways

You can draw income payments out of a fixed annuity three (3) ways:

1. By taking periodic withdrawals from time to time as you need income.

2. Change the annuity from a deferred annuity into an income annuity like a Single Premium Immediate Annuity (SPIA) by annuitizing it, and give the cash value to the insurance company.

3. Activate an annuity income rider and take off an income for life while maintaining access to the cash value.

What is an Income rider?

The lifetime income rider is a feature that can be added to an annuity but at an additional cost. It provides a contractually guaranteed future lifetime income at a date chosen by you. Also, the rider provides you with a formula for calculating your future income.

The BIG reason is Liquidity

With an income annuity like a Single Premium Immediate Annuity (SPIA), a Deferred Income Annuity (DIA) or a Qualified Longevity Annuity Contract (QLAC), you give your money to the insurance company and in most cases cannot get it back. There is no cash value. Deferred fixed annuities have a cash value that you can access. However, by using the annuity income rider the deferred fixed annuity can provide you with income like a SPIA, DIA, or QLAC income annuity, could.

Here’s the catch:

Because you have access to the cash value, expect the income rider on any deferred annuity to pay less income than a typical income annuity. In other words, if you want maximum income for the least amount of money, you should consider an income annuity such as a Single Premium Immediate Annuity (SPIA), a Deferred Income Annuity (DIA) or a Qualified Longevity Annuity Contract (QLAC).

Buying an annuity with a lifetime income rider

If you want to buy a deferred annuity with a lifetime income rider, you could buy it with:

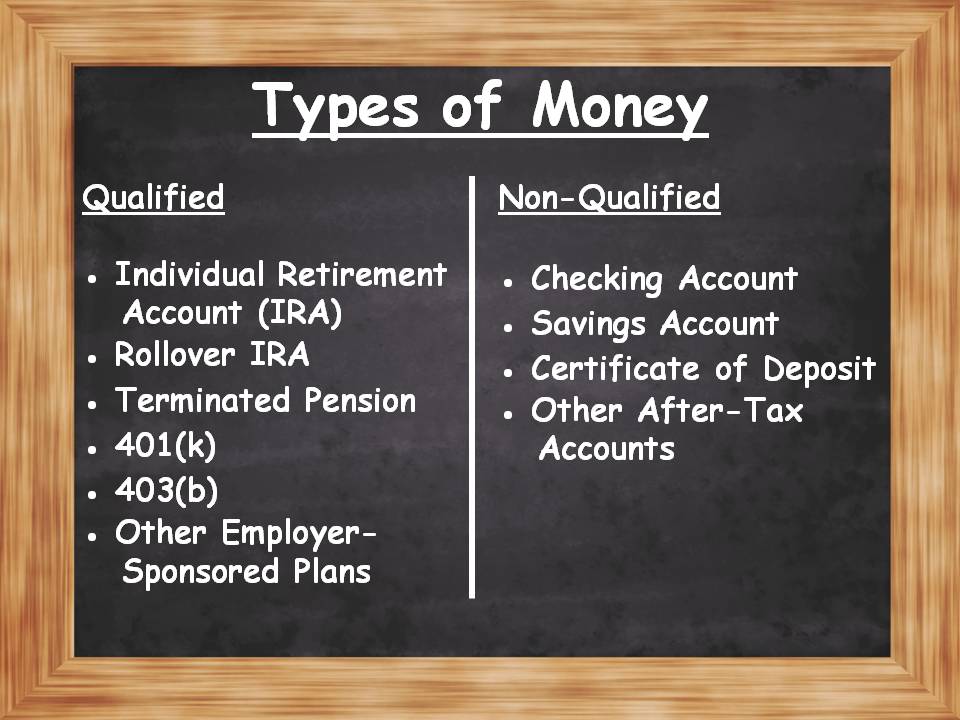

1. Non Qualified funds – a non-IRA bank checking account, savings account, Certificate of Deposit (CD), etc.

2. Qualified funds – an Individual Retirement Account (IRA), an IRA rollover, a terminated pension, a 401(k), a 403(b) or other employer-sponsored retirement plans.

How does lifetime income work?

You put a deposit known as a premium payment with the insurance company. In most cases, you must request the annuity income rider at the time of purchase. For most riders, each year you do not access the income, the income “roll-up rate” or payout amount goes up, regardless of actual annuity earnings. Usually, the formula used to calculate your income will often exceed what you earn on your money. Not all insurance companies offer lifetime income riders.

Then in the future

When you start taking your lifetime income using the annuity income rider, the amount of income you receive is subtracted from your account balance. Your account balance will go down if earnings are less than the income paid to you. However, you can access the remaining cash value balance of your annuity at any time. Consequently, a cash value withdrawal more than the income payment will reduce the amount of your income future payments.

When you start taking your lifetime income using the annuity income rider, the amount of income you receive is subtracted from your account balance. Your account balance will go down if earnings are less than the income paid to you. However, you can access the remaining cash value balance of your annuity at any time. Consequently, a cash value withdrawal more than the income payment will reduce the amount of your income future payments.

Run out of money, not income.

If you live a long life, and your annuity lifetime income payment and rider fee have caused your annuity cash value balance to drop to zero ($0), then income drawn from your lifetime income rider will continue. The rider provides your lifetime income. In this case, there would be nothing to pass on to your heirs, but you also have protected yourself from living too long. Your income will continue.

What does this mean

What does this mean

Expect your cash value to go down as you take income. It is highly unlikely that interest earned in a deferred fixed annuity will exceed combined cost of the lifetime income rider fee and the income itself.

Riders are not free

The lifetime income rider is a feature added to the annuity at an additional cost. So, an annuity income rider typically will cost somewhere between half a percent (½%) and one percent (1%) per year. Since there is a fee, you can receive a guaranteed future lifetime income backed by the full faith and credit of the insurance company you chose. Except for the income rider fee, there are usually no annual fees for having a deferred fixed annuity.

The lifetime income rider is a feature added to the annuity at an additional cost. So, an annuity income rider typically will cost somewhere between half a percent (½%) and one percent (1%) per year. Since there is a fee, you can receive a guaranteed future lifetime income backed by the full faith and credit of the insurance company you chose. Except for the income rider fee, there are usually no annual fees for having a deferred fixed annuity.

Do not confuse cash value with roll-up value

Many agents do not explain the future income formula well, so many clients have the misunderstanding that while they are not taking any income from their annuity, they are earning a guaranteed five percent (5%) or more interest rate on their money. Some insurance company annual statements are not very clear on this point either. The bottom line, the roll-up rate is not your money.

It’s like this

It’s like this

If you have a credit card with airline frequent flyer miles, those miles can only purchase a plane ticket. You cannot spend airline frequent flyer miles on food, gas, gifts or anything else, only plane tickets. Your rollup value on your statement is not your money; it is a part of the formula for calculating future income only. Furthermore, you cannot spend your rollup amount on food, gas, gifts, bills or anything else.

Spousal Coverage

Some insurance companies provide a joint rider that covers two people. The revenue stream continues until the last person is gone. At that point, any remaining cash value in the annuity would pass to the named beneficiaries.

Inflation Protection

Some insurance companies also offer the choice of receiving an inflation-protected income. Accepting Inflation protection usually means that you start taking a lower amount of income that increases over time. Before choosing this option, you should understand the inflation formula and how it works when compared a payout with no inflation protection.

You maintain Control of your money

When you give your money to the insurance company to buy any deferred annuity with an income rider, your money is still available to you. A deferred annuity such as a fixed annuity provides you with:

When you give your money to the insurance company to buy any deferred annuity with an income rider, your money is still available to you. A deferred annuity such as a fixed annuity provides you with:

• Liquidity.

• A cash surrender value.

• Growth potential.

Why is that important?

Payments made into an income annuity like a Single Premium Immediate Annuity (SPIA), a Deferred Income Annuity (DIA), or a Qualified Longevity Annuity Contract (QLAC), are not accessible as cash, only as income. You can access the cash value of a fixed and fixed index annuity. That cash value could also be used to provide income using a lifetime income rider or by annuitizing the contract.

What is the Return On Investment (ROI)?

What is the Return On Investment (ROI)?

The best feature of any deferred fixed annuity is the ability to know at any time what minimal interest you can expect to receive. However, the actual earnings may be higher depending on potential future rate increases that are not guaranteed.

Surrender penalties, periods and charges

A bank Certificate of Deposit (CD) has a penalty for early withdrawal if you take out more than the interest before maturity. A penalty for early withdrawal in a fixed annuity is known as a surrender charge. However, income taken from an annuity using an income rider is typically surrender charge free.

We can’t emphasize this enough

Withdrawals from a fixed or fixed index annuity before age 59½ could be subject to an additional 10% federal income tax penalty on any gain.

Start at the finish

Start at the finish

The best way to buy any deferred annuity with a lifetime income rider is with the end result in mind. Start with a budget. Set some goals or perhaps create a bucket list. Figure out how much you need on a monthly basis to protect your lifestyle. Subtract out Social Security and pension. You might want to purchase a deferred fixed annuity with an income rider to cover some or all of the remaining expenses.

The Key to figuring it out is

If you are like most people, you probably need additional information to help you plan your retirement lifestyle and determine if a Qualified Longevity Annuity Contract is right for you. As a Bonus, we have created a guide to help you called “Start at the Finish Line”. It contains information to help you set goals and plan for the retirement lifestyle that you are looking for.

Avoid Banks, Brokers, and Captive Agents

Find an independent financial professional that is not tied to a bank, brokerage house or insurance company. Bankers, brokers and captive agents generally have a limited inventory of annuities with income riders to offer. Independent financial professionals can generally offer you more choices.

Spend no more than you actually need

If you need $2,322 per month more, buy that exact amount, not a penny more. Purchase your annuity from a highly rated company, maybe more than one. Let the insurance company become responsible for you living too long.

This is important

Remember that the income payments are backed by the financial strength and claims-paying ability of the insurance company or companies you chose. Therefore, it may be in your best interest to choose a highly rated company, or better yet, multiple companies. You can check ratings from sources like AM Best, Fitch, Moody's and Standard and Poor’s.

Also

Do not spend everything you have on a deferred fixed annuity with an income rider. Before buying one, you should set aside adequate cash reserves to meet unexpected bills and emergencies. The general rule of thumb is about one year of income. Anything more and you probably are missing a financial opportunity.

Do not spend everything you have on a deferred fixed annuity with an income rider. Before buying one, you should set aside adequate cash reserves to meet unexpected bills and emergencies. The general rule of thumb is about one year of income. Anything more and you probably are missing a financial opportunity.

In Conclusion

Having an annuity income rider on a deferred fixed annuity can provide you a lifetime of income you cannot outlive. You keep the right to use to your cash value, maintain your safety of principal with interest paid on a tax-deferred basis. If you do not have a pension and want one, a lifetime income rider could become your personal pension, private pension or do-it-yourself pension.

Finally

If you are at or near retirement and you have any questions about how annuity income riders work on deferred fixed annuities or just need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

KEY BENEFITS

- Principle protection.

- Tax-deferred accumulation.

- Income for life.

- A guaranteed minimum rate of return.

- A way to calculate the contract surrender value at any time.

Articles