Traditional Fixed Annuity

What is a Traditional Deferred Fixed Annuity?

Think of a Traditional Deferred Fixed Annuity like a savings account in the bank. They are both savings vehicles, they both pay interest, but that’s where the similarities end. A Traditional Deferred Fixed Annuity offers an interest rate guarantee period that is good for one year at a time but is less liquid than a bank account. Your principal is kept protected and the interest earned is tax-deferred (taxes are not due) until the earnings are taken out.

Think of a Traditional Deferred Fixed Annuity like a savings account in the bank. They are both savings vehicles, they both pay interest, but that’s where the similarities end. A Traditional Deferred Fixed Annuity offers an interest rate guarantee period that is good for one year at a time but is less liquid than a bank account. Your principal is kept protected and the interest earned is tax-deferred (taxes are not due) until the earnings are taken out.

What this means is

A Traditional Deferred Fixed Annuity or Traditional Fixed Annuity is a savings vehicle from an insurance company that provides principle protection of your money. You can buy it with a lump sum payment or with installment payments. Your Traditional Fixed Annuity is designed to pay you a competitive rate of return good for one year. The renewal interest rate should be reasonable compared with prevailing rates but guaranteed to be no less than contractually guaranteed minimum renewal rate after the first year.

Why are these less popular?

Many people like bank Certificate of Deposits (CD’s) because they know what interest rate they will get for the period they hold their CD. In most Traditional Fixed Annuities, you only are aware of the interest rate for the first year. People who favor bank Certificates of Deposit (CD’s) tend to prefer the Multi-Year Guaranteed Annuity (MYGA) that also pay a contractually guaranteed level interest rate, but for a set time period.

Why would I buy one?

In a rising interest rate environment like we have seen in 2017, your traditional fixed annuity interest rate should increase at the end of the annuity anniversary. The renewal rate could potentially pay you more than money trapped in a bank Certificate of Deposit or an insurance company Multi-Year Guarantee Annuity. However, if prevailing rates later decrease, your earnings should decline as well.

In a rising interest rate environment like we have seen in 2017, your traditional fixed annuity interest rate should increase at the end of the annuity anniversary. The renewal rate could potentially pay you more than money trapped in a bank Certificate of Deposit or an insurance company Multi-Year Guarantee Annuity. However, if prevailing rates later decrease, your earnings should decline as well.

The other reason to buy one.

Many Traditional Fixed Annuities come with an optional lifetime income rider. When activated, the rider will pay you, or you and another person, a lifetime income, no matter how long you live, even if you balance goes to zero. At death, anything left over goes to your beneficiaries.

Many Traditional Fixed Annuities come with an optional lifetime income rider. When activated, the rider will pay you, or you and another person, a lifetime income, no matter how long you live, even if you balance goes to zero. At death, anything left over goes to your beneficiaries.

Why is this important?

If you want access to your cash value while you are receiving an income from a lifetime income rider, a fixed annuity with an income rider can provide that access. However, if you take money out, you will also be reducing your payment amount too. The amount you withdraw determines the reduction.

As a savings vehicle, where do you start?

There are two ways to buy a Traditional Fixed Annuity:

- With a single premium amount to an insurance company into a Single Premium Deferred Annuity (SPDA). One payment is more common in today’s low-interest-rate environment.

- With installment payments to an insurance company into a Flexible Premium Deferred Annuity (FPDA). The FPDA is hard to find but is usually available in an employer-sponsored payroll deduction retirement plans.

What can I buy a Traditional Fixed Annuity with?

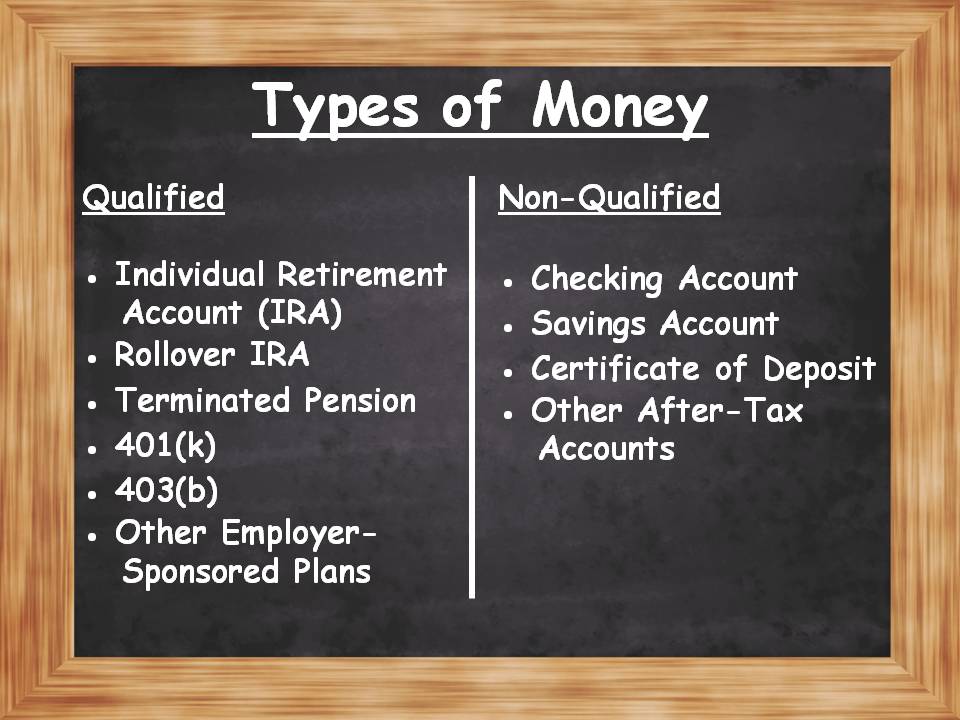

If you want to buy a fixed annuity you could use your saving from one of two places:

- Non Qualified funds – a non-IRA bank checking account, savings account, Certificate of Deposit (CD), etc.

- Qualified funds – an Individual Retirement Account (IRA), an IRA rollover, a terminated pension, a 401(k), a 403(b) or other employer-sponsored retirement plans.

You maintain Control of your money

When you give your money to the insurance company to buy a fixed annuity, your money is still available to you. Your fixed annuity provides you with:

• Liquidity.

• A cash surrender value.

• Growth potential.

Why is that important?

Deposits made into a Single Premium Immediate Annuity (SPIA), a Deferred Income Annuity (DIA), or a Qualified Longevity Annuity Contract (QLAC), are not accessible as cash, only as income. You can access the cash value of deposits in a Traditional Fixed Annuity. The cash value of a Traditional Fixed Annuity could also be received as income using a lifetime income rider or by annuitizing the contract.

What is the Return On Investment (ROI)?

The best feature of a Traditional Fixed Annuity is the ability to know at any time what minimal interest you can expect to receive. However, the actual earnings may be higher depending on potential future rate increases that are not guaranteed.

The best feature of a Traditional Fixed Annuity is the ability to know at any time what minimal interest you can expect to receive. However, the actual earnings may be higher depending on potential future rate increases that are not guaranteed.

Fee Free

In the past, it was extremely unusual to find a fixed annuity with an annual fee. We do not know of any traditional fixed annuities that are issued today that have an annual fee. However, if you add an income rider or other feature to your annuity, a fee comes with those riders. If you want to use a Traditional Fixed Annuity to save safely only, avoid the riders to avoid the fees.

In the past, it was extremely unusual to find a fixed annuity with an annual fee. We do not know of any traditional fixed annuities that are issued today that have an annual fee. However, if you add an income rider or other feature to your annuity, a fee comes with those riders. If you want to use a Traditional Fixed Annuity to save safely only, avoid the riders to avoid the fees.

If I made a single payment, what do I get?

Most Traditional Fixed Annuities purchased with a single premium, pay an interest rate that is good for one year, then renew at a current rate decided by the insurance company. Some companies might also pay a bonus rate in the first year, or have an introductory period for more than one year. The renewal rate will typically be no less than the contractual minimum set in the annuity contract.

What this means is:

The renewal rate is at the discretion of the insurance company, so choose a good one that has a solid renewal rate history. However, your contract has a minimum renewal interest rate that the company must pay you. This minimum interest is usually between a quarter of one percent (¼%) to one percent (1%).

The good news is

In a rising interest rate environment, most annuities will renew above the stated minimum interest rate in the contract. So if the prevailing interest rates have gone up since you bought your fixed annuity, your interest rates should go up with the current rates. Of course, if rates remain the same or go down you can count on receiving no less than the minimum interest rate stated in your contract.

But the real cool part is you postpone taxes

If you buy a non-qualified fixed annuity with non-qualified money, your interest accumulates tax-deferred. That means you do not have to pay taxes on the interest earned if you do not withdraw it. Then your entire interest earned from the prior year can also earn more interest, also tax-deferred until you take it.

What that means is

You could compound interest on interest in your Traditional Deferred Fixed Annuity, and defer paying taxes on the earnings until withdrawn. Interest earned in the bank is taxed every year whether you take it out or not.

And that could mean lower taxes

If you are at what accountants call the “tipping point,” having some of your interest tax-deferred can mean fewer taxes. If you are over the tipping point, some deductions are no longer available to you, and you ended up paying Uncle Sam more money. Sometimes by simply moving money into a tax-deferred fixed annuity can make a world of difference.

If you are at what accountants call the “tipping point,” having some of your interest tax-deferred can mean fewer taxes. If you are over the tipping point, some deductions are no longer available to you, and you ended up paying Uncle Sam more money. Sometimes by simply moving money into a tax-deferred fixed annuity can make a world of difference.

Avoid Probate Court

Whatever you have in your annuity passes directly to a named beneficiary or beneficiaries, by contract, and usually avoids probate court. Your heirs receive whatever is in your Traditional Fixed Annuity at your demise. In fact, some companies allow a spouse or children to continue the annuity as an annuity, instead of cashing it out.

Some insurance companies even pay a bonus

Some insurance companies will pay a bonus in the first year, sometime over the first few years. That can be a good idea as long as you know the terms and conditions. The bigger the bonus, the more likely you will only earn the contractual minimums after the initial interest rate period.

What is the alternative to a bonus annuity?

Sometimes the better choice is to take a contract with a lower bonus or no bonus and look for certain key contractual benefits:

• High contractual minimum interest rate.

• Short surrender schedule.

• Low surrender charges.

• No Market Value Adjustment (MVA).

Market Value What?

Some Traditional Fixed Annuities come with a Market Value Adjustment (MVA). An MVA adjusts the withdrawal value of a contract if prevailing interest rates changed since purchase. If rates have gone up, the value of the contract is adjusted downward. If rates have gone down, the value is adjusted upward. An MVA usually applies only during the surrender period.

Surrender penalties, periods and charges

A bank Certificate of Deposit (CD) has a penalty for early withdrawal if you take out more than the interest before maturity. A penalty for early withdrawal in a fixed annuity is known as a surrender charge. A surrender charge is accessed on any amount withdrawn more than the free withdrawal amount, during the surrender period.

Here's the deal:

Most Traditional Fixed Annuities have surrender charge periods ranging for five (5) to ten (10) years. While banks may only allow you access to the interest earned without penalty, in a Traditional Deferred Fixed Annuity you can usually withdraw up to ten percent (10%) of the contract value after the first year, without an additional penalty for early withdrawal.

Even better because

By using the surrender charge schedule and the contractually guaranteed minimum interest rate, you can calculate what the minimum you will have in your account at any point in time.

Annuitization

Traditional Fixed Annuities typically provide you an option to convert to an immediate income annuity at no cost to you. When you annuitize your deferred fixed annuity to an income annuity, you are turning your money into a series of income payment, possibly for life. You should check with your insurance company about the payout options.

Traditional Fixed Annuities typically provide you an option to convert to an immediate income annuity at no cost to you. When you annuitize your deferred fixed annuity to an income annuity, you are turning your money into a series of income payment, possibly for life. You should check with your insurance company about the payout options.

Here’s the annuitization catch

One of the reasons you probably chose the Deferred Fixed Annuity is to have access to your cash. When converted to an income annuity, you lose access to that cash by handing it over to the insurance company for the promise of income payments. That means you will only get back income, and your heirs can get whatever is left over (if any) only if you use a refund or installment payout.

The income rider as an Annuitization Alternative

If you need full control of your money and yet want a future income guarantee, then you probably want a Traditional Deferred Fixed Annuity with a lifetime income rider. The rider can provide a lifetime of income for you and sometimes for you and another person.

We can't emphasize this enough:

Withdrawals from a Traditional Fixed Annuity before age 59½ could be subject to an additional 10% federal income tax penalty on any gain.

In Conclusion

The Traditional Fixed Annuity is a great choice in a rising interest rate environment. You have access to your cash value and your principal is protected and interest is paid on a tax-deferred basis. There are no annual fees.

Finally

If you are at or near retirement, and you have any questions about Traditional Fixed Annuities or just need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

KEY BENEFITS

- No annual fees.

- Principle protection.

- Tax deferred accumulation.

- The option to earn a guaranteed income for life.

- A guaranteed minimum rate of return.

- A way to calculate the contract surrender value at any time.

Articles

For Additional Information Request Your Guide to Saving Safely: