Single Premium Immediate Annuity (SPIA)

What is a Single Premium Immediate Annuity (SPIA)?

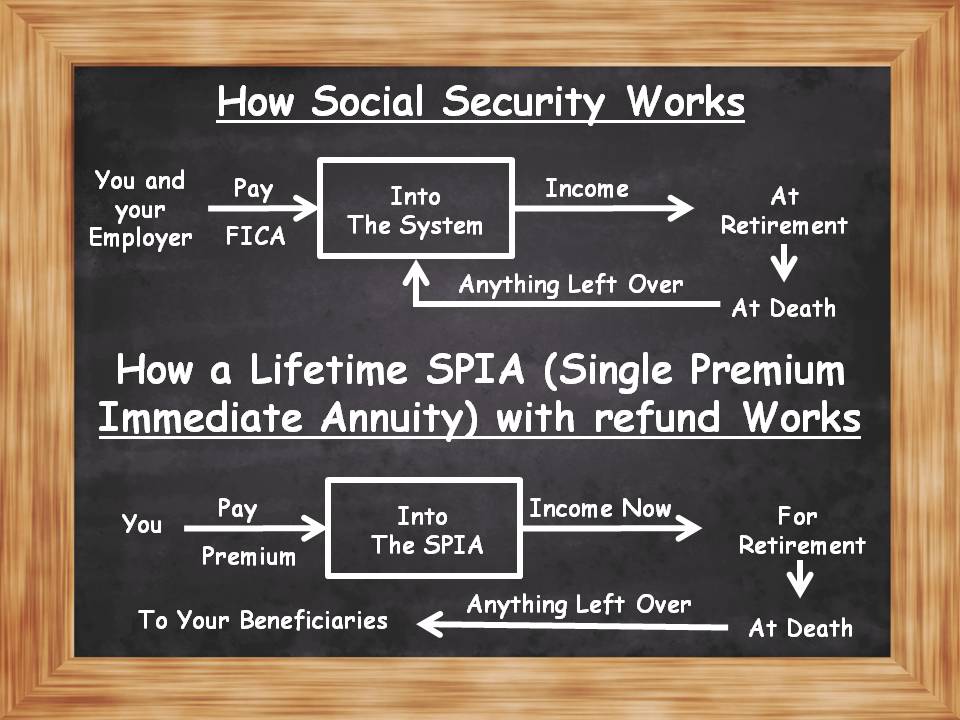

If you are retired and receiving a Social Security check, it is like having a lifetime income from a Single Premium Immediate Annuity (SPIA). Unlike Social Security that you paid into over your working years, a Single Premium Immediate Annuity can turn your one-time payment into a lifetime of income.

If you are retired and receiving a Social Security check, it is like having a lifetime income from a Single Premium Immediate Annuity (SPIA). Unlike Social Security that you paid into over your working years, a Single Premium Immediate Annuity can turn your one-time payment into a lifetime of income.

The SPIA is older than Social Security

In fact, the Single Premium Immediate Annuity is older than Social Security. Social Security was signed into law in 1935 and payments began in 1940. The Single Premium Immediate Annuity can trace its roots back to the Roman Empire.

In fact, the Single Premium Immediate Annuity is older than Social Security. Social Security was signed into law in 1935 and payments began in 1940. The Single Premium Immediate Annuity can trace its roots back to the Roman Empire.

The SPIA dates back to ancient Rome

Back in ancient Rome, “annua” were used to provide income payments over a set number of years or for life. Essentially, a Single Premium Immediate Annuity is the oldest way you could guarantee yourself an income for life.

Like Social Security, A SPIA can pay an income for life

A Single Premium Immediate Annuity can be designed to pay you a single or joint lifetime income. That means it can work almost identically to receiving a Social Security check in retirement. You can also choose shorter payment periods too.

A SPIA is a reliable source of immediate Income

You make a single premium payment into a Single Premium Immediate Annuity (SPIA), and the annuity turns it into immediate income for you or you and someone else, possibly income for life, if so desired. If you need income right now or within the next 12 months, you might want to consider using a Single Premium Immediate Annuity.

How does Social Security Compare?

How does Social Security Compare?

Social Security takes a lifetime of payments during your working years from you and your employer, then at retirement, turns those payments into immediate lifetime income. Of course, you also have to be able to qualify for it. Basically, the risk of you living a long life has been transferred to the government.

How does a Pension compare?

A pension takes a lifetime of payments during your working years from your employer, then at retirement, turns those payments into immediate lifetime income. All the risk of a pension payment is with your employer, but pensions are usually insured by the federal government. If you do not have a pension and are retired and need one, a Single Premium Immediate Annuity may be the best solution for a personal or private pension or a do-it-yourself pension.

Lotteries use Immediate Income Annuity payments

Lotteries use Immediate Income Annuity payments

If you have ever won the jackpot of Mega Millions or Powerball, you know you have two ways to claim the jackpot prize. You can take your winnings as a lump sum, or in the form of an annuity. The annuity amount is in essence, a payment like a Single Premium Immediate Annuity payment.

What’s the real story?

The only thing worse than dying is outliving your money. As you think about your retirement, does it seem more likely your money will outlive you, or you will outlive your money? Income annuities like the Single Premium Immediate Annuity are the only thing we know of that an individual or couple could purchase to provide a lifetime of income, or a shorter time frame if desired. With a lifetime benefit, you are essentially transferring the risk of living a long life to an insurance company.

But first, you have to buy a Single Premium Immediate Annuity from an insurance company. But that’s not how we were trained by those who love us the most. Ever since we were young, our parents taught us that if we ever had two nickels to rub together, they belonged in a FDIC insured account in the bank.

Unfortunately chasing x percent around in the bank seems to be a sure-fire way to go broke safely. You cannot run out of money if you have a lifetime of income guaranteed by the insurance company. Plus you are taking advantage of the insurance company’s mortality credits and hedging strategy.

The real challenge is:

Even though pensions are disappearing, many retirees continue to focus on the size of their stack of money and not what their money can do for them. For some, having a large pile of cash chasing x percent return is more important than having an enjoyable retirement that a Single Premium Immediate Annuity can contribute to.

Even though pensions are disappearing, many retirees continue to focus on the size of their stack of money and not what their money can do for them. For some, having a large pile of cash chasing x percent return is more important than having an enjoyable retirement that a Single Premium Immediate Annuity can contribute to.

So where do you start?

You purchase your Single Premium Immediate Annuities from an insurance company. You make a lump sum premium payment into the Single Premium Immediate Annuity. Then you chose how you want to receive your money.

The best part is

The insurance company is then on the hook to provide the promised income payment for you. Essentially you are transferring your risk of living too long to the insurance company.

The best choice for lifetime income is…

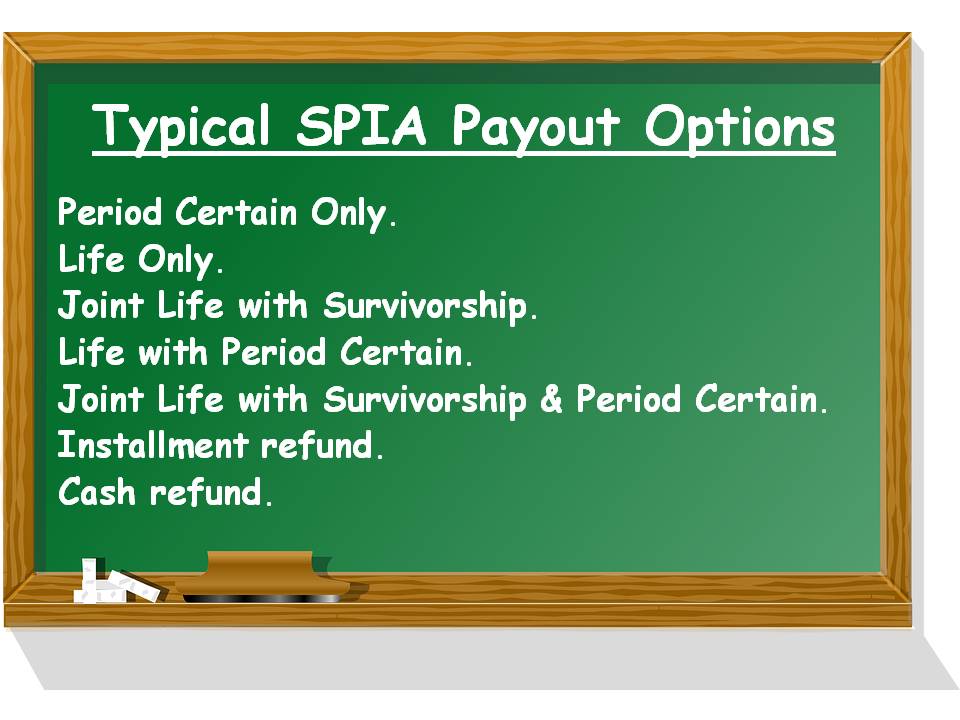

The popular choice is the joint life with survivorship or single life either with a cash refund or installment refund to heirs. This selection provides you a lifetime of income no matter how long you live (for a single life) or you both live (for a joint life). If you die young and there is anything left over, your beneficiaries will get it.

And the great mystery is

So what do you want your beneficiaries to have?

- All the money right away (cash refund).

- The same payment until the premium is gone (installment refund).

The answer may depend on how your heirs handle their money currently.

If you want maximum income. . .

Of course, you could choose the life only joint life with survivorship or single life only payment. That way you would get the largest payment of a lifetime of income no matter how long you live (for a single life) or you both live (for a joint life). A payment while alive is kind of how Social Security works in retirement. When you die, there is no more money paid out. In this case, if you die young and there is anything left over, the insurance company keeps it.

We do not recommend this

We do not recommend this

In a joint payout, you could have a payment reduction at the death of the first person. While you get more when both people are alive, a decrease in income can shortchange the survivor. Most people prefer a joint 100% payment for each person.

Would you prefer a more limited income?

If you do not want an income for life, you can choose to receive it for a certain period such as five to twenty years, or somewhere in between. That means the payment is made to you or your beneficiary for the period of time you chose, then stops at the end of that period.

Would you like a combo?

Of course, you could always go for the combination of the single life or joint life with survivorship and a period certain. This choice provides a lifetime of income no matter how long you live (for a single life) or you both live (for a joint life). If you die young, payments continue until the end of the stated period. If you live past the period then die, your heirs will get nothing.

Here’s the deal:

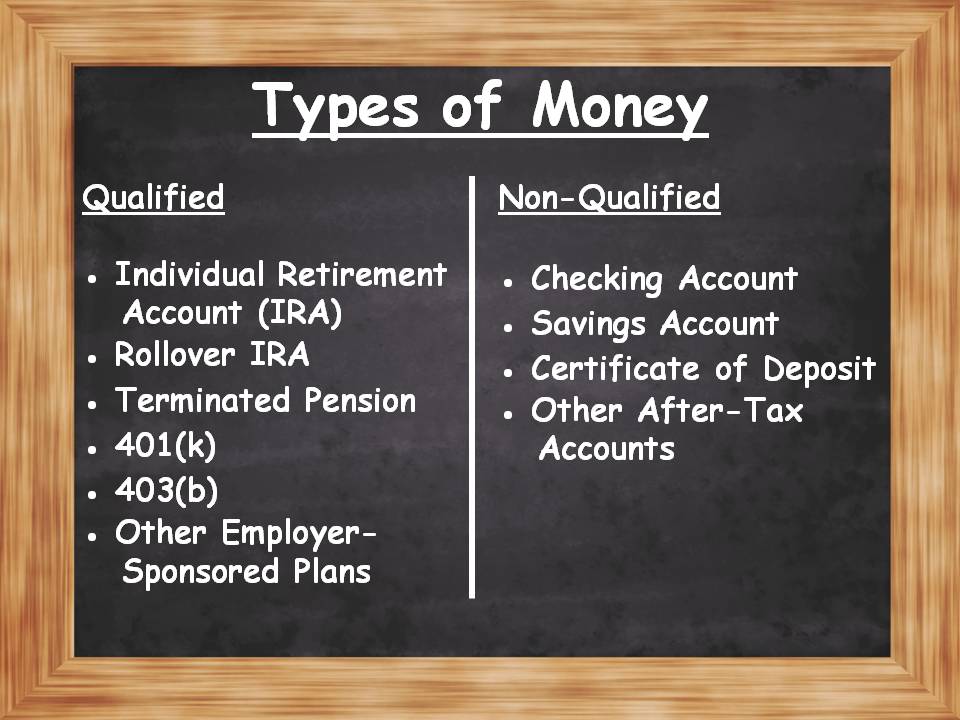

You can purchase a Single Premium Immediate Annuity using what is called non-qualified money. That’s money from a non-IRA checking, savings, Certificate of Deposit (CD), etc. When you do this, you can take advantage of the exclusion ratio. The exclusion ratio could lower your taxes by paying you a higher non-taxable payment for a period of time.

But wait! There’s more:

You can also buy a Single Premium Immediate Annuity using qualified money from a(n):

- Individual Retirement Account (IRA)

- IRA rollover

- Terminated pension

- 401(k)

- 403(b)

- other employer-sponsored plans.

Sadly, Uncle Sam will want you to pay taxes on every dollar you get from any qualified funds. So the entire income you receive from your SPIA funded with qualified money will be fully taxable.

You have no fees

You have no fees

On the positive side, a Single Premium Immediate Annuity has no annual fees. A Single Premium Immediate Annuity is all about income. You get an income based on the customizable income benefit you choose. There are no fees.

You have no market risk

Income from a Single Premium Immediate Annuity does not have any market risk. A SPIA can provide correction protection. An unfortunate sequence of returns, where you retire and lose a lot of money on Wall Street early on in retirement, could cripple your retirement plans. A steady immediate income could be a better choice.

What that means is:

What that means is:

Unlike money in the bank or on Wall Street, with a Single Premium Immediate Annuity, you do not need to worry about chasing x percent return that cannot be guaranteed. You are guaranteed the income you chose. If you choose a lifetime income, you will get an income you cannot outlive. You have transferred the risk of living too long to the insurance company.

Your income can increase each year

Your income can increase each year

Want to fight inflation? Then purchase your Single Premium Immediate Annuity with a Cost Of Living Adjustment (COLA) rider. You chose the percentage increase (like 1% to 5%), and that is the set amount your income will increase each year.

Or you can skip the flat amount and…

Instead of buying a set amount for inflation protection you might choose the CPI-U rider. The yearly income increase will be determined by the Consumer Price Index for All Urban Consumers and may vary based on the index.

You can wait up to 12 months to get your first check.

Ironically the name Single Premium Immediate Annuity implies you must take your income immediately. You can wait up to twelve months before you start taking income.

Choose, but chose wisely.

When you buy a Single Premium Immediate Annuity, you are giving your money to an insurance company who in return gives you a promise to pay you the income you chose. You are purchasing that revenue with a lump sum payment. A Single Premium Immediate Annuity usually has:

- No cash surrender value.

- No accumulation value.

- Zero Liquidity.

- No growth potential

Why is this important?

For almost all Single Premium Immediate Annuities, once you give the insurance company your money and start the contract, you cannot get your money back. However, in exchange for your premium, you will know exactly what income you will receive.

But then again if your Social Security and pension are not paying your essential bills, maybe a Single Premium Immediate Annuity is right for you. If you retired without a pension, it is definitely the right choice for a private or personal pension or do-it-yourself pension.

What is the Return On Investment?

What is the Return On Investment?

If you have a birth certificate with an expiration date on it, it is easy to figure out what your return on investment will be. Since expiration dates on birth certificates do not exist, there is no way to calculate your Return On Investment (ROI) until death. Since there is no cash surrender value in a Single Premium Immediate Annuity, there is no chasing x percent return that cannot be guaranteed. Therefore, there is no ROI.

Be Advised:

Withdrawals from a Single Premium Immediate Annuity before age 59½ could be subject to an additional 10% federal income tax penalty on any gain.

Start at the Finish

Start at the Finish

The best way to buy a Single Premium Immediate Annuity is with the end result in mind. Start with a budget. Set some goals or perhaps create a bucket list. Figure out how much you need on a monthly basis to protect your lifestyle. Subtract out Social Security and pension. You might want to purchase a SPIA to cover some or all of the remaining expenses.

The key to figuring it out is

If you are like most people, you probably need additional information to help you plan your retirement lifestyle and determine if a Single Premium Immediate Annuity is right for you. As a Bonus, we have created a guide to help you called “Start at the Finish Line.” It contains information to help you set goals and plan for the retirement lifestyle that you are looking for.

Avoid Banks, Brokers, and Captive Agents

Find an independent financial professional that is not tied to a bank, brokerage house or insurance company. Bankers, brokers and captive agents generally have a limited inventory of Single Premium Immediate Annuities to offer. Independent financial professionals can generally offer you more choices.

Spend no more than you actually need

Spend no more than you actually need

If you need $2,322 per month more, buy that exact amount, not a penny more. Purchase your Single Premium Immediate Annuity from a highly rated company, maybe more than one. Be careful not to put too much into a SPIA. Let the insurance company become responsible for you living too long.

We can’t Emphasize this enough

Remember that the income payments are backed by the financial strength and claims-paying ability of the insurance company or companies you chose. It may be in your best interest to choose a highly rated company, or better yet, multiple companies. You can check ratings from sources like AM Best, Fitch, Moody's and Standard and Poor’s.

Also

Do not spend everything you have on a Single Premium Immediate Annuity. Before buying a Single Premium Immediate Annuity, you should set aside adequate cash reserves to meet unexpected bills and emergencies. The general rule of thumb is about one year of income. Anything more and you probably are missing a financial opportunity.

Request a Quote to see actual dollar amounts:

- Based on your specific dollar amount or a lump sum payment. We would then look for the insurance company that pays you the maximum monthly income for that amount.

- Based on your desired monthly income amount. We would then look for the insurance company that provides you that income for the smallest lump sum payment.

We normally quote lifetime benefits, but you can request a shorter income payment period.

In Conclusion

The Single Premium Immediate Annuity (SPIA) can guarantee you an immediate retirement income that you cannot outlive, or a shorter period if desired. A SPIA can provide additional income beyond what is provided from Social Security and a pension. If you do not have a pension and would like one, a SPIA can become your private or personal pension or a do-it-yourself pension.

Finally

If you are at or near retirement, and you have any questions or need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

KEY BENEFITS

- No annual fees.

- Fixed monthly lifetime income payments can begin immediately and never change regardless of market conditions.

- Solves the risk of outliving your money.

- Optional “Cash Refund” feature guarantees your heirs won’t lose a penny of your premium if you die too soon.

- Optional Cost Of Living Adjustment (COLA) can be added.

Articles