Qualified Longevity Annuity Contract (QLAC)

What is a Qualified Longevity Annuity Contract (QLAC)?

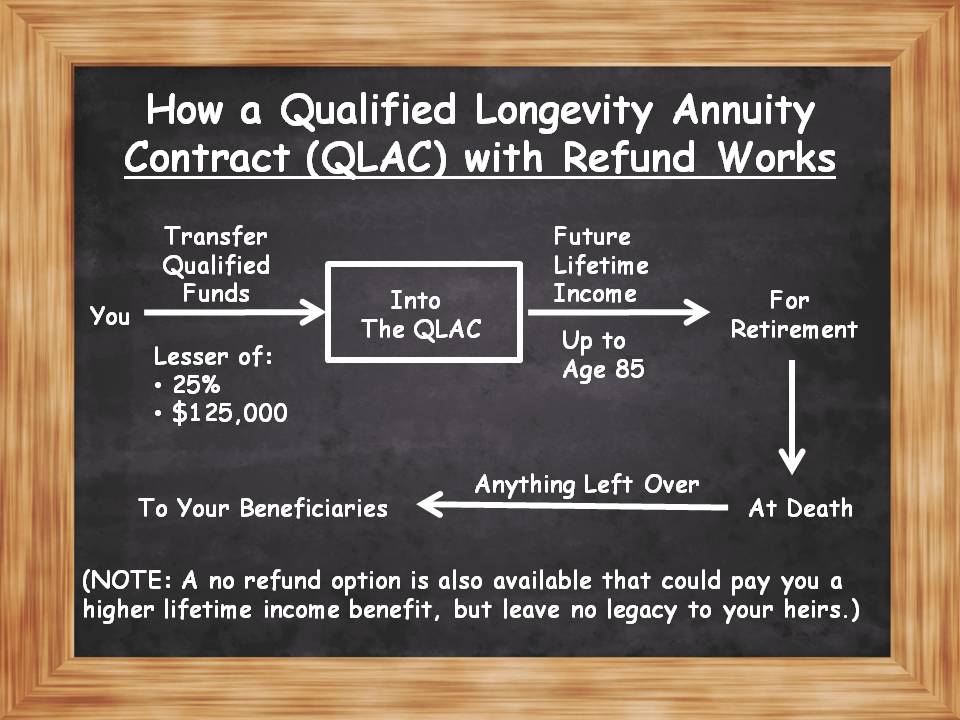

A Qualified Longevity Annuity Contract (QLAC) is a unique type of Deferred Income Annuity (DIA) or Longevity Annuity funded by an IRA or another qualified plan. It provides you a future pension-like income at a date you choose. It can help you postpone paying taxes on a portion of your qualified money until age 85.

A Qualified Longevity Annuity Contract (QLAC) is a unique type of Deferred Income Annuity (DIA) or Longevity Annuity funded by an IRA or another qualified plan. It provides you a future pension-like income at a date you choose. It can help you postpone paying taxes on a portion of your qualified money until age 85.

Why would I want a Qualified Longevity Annuity Contract (QLAC)?

A Qualified Longevity Annuity Contract (QLAC) might be right for you if:

- You are retiring soon or retired and living comfortably on your Social Security and/or a pension.

- You do not need money from your IRA, 401k, 403b or another qualified plan to live on.

- If you are in good health.

- Have longevity in your family history.

Postponing Required Minimum Distributions (RMD’s)

The Qualified Longevity Annuity was created to help people defer paying Required Minimum Distributions (RMD's) on a portion of their qualified money. You can delay taking RMD’s from up to 25% of your qualified retirement plans to a maximum of $125,000, whichever is less. Income withdrawals can be deferred up to age 85, or sooner if you desire.

The Qualified Longevity Annuity was created to help people defer paying Required Minimum Distributions (RMD's) on a portion of their qualified money. You can delay taking RMD’s from up to 25% of your qualified retirement plans to a maximum of $125,000, whichever is less. Income withdrawals can be deferred up to age 85, or sooner if you desire.

The Qualified Longevity Annuity Contract was invented in 2014

You have probably never heard of it because it was not around four years ago. On July 1, 2014, the Internal Revenue Service (IRS) and Treasury department came together to create the rules and regulations that created the QLAC. The QLAC just celebrated its 3rd birthday.

You have probably never heard of it because it was not around four years ago. On July 1, 2014, the Internal Revenue Service (IRS) and Treasury department came together to create the rules and regulations that created the QLAC. The QLAC just celebrated its 3rd birthday.

Avoid a QLAC if you need everything to live on

If you need your Social Security, pension and money from your retirement plan to live on while you are retired, you probably do not need a Qualified Longevity Annuity contract. If you are already taking and spending your Required Minimum Distribution to pay your bills, buying a QLAC is unlikely to help you. You should only transfer any surplus qualified funds that you do not need to take money from into a QLAC.

About RMD’s

In a traditional IRA like other qualified plans, the Required Minimum Distributions (RMDs) must be taken by the year after you turn 70½, whether you need them or not. In a Qualified Longevity Annuity Contract, you can defer RMD payments until age 85. Deferring to age 85 means that you do not need to pay any taxes on the money you have in your Qualified Longevity Annuity Contract at age 70½.

The real reason to buy a QLAC

The best reason to buy a QLAC is for the future guaranteed income. While you do get the benefit of postponing Required Minimum Distributions on a portion of your money, the real benefit is the future income. The income payout increases every year of deferral, and the insurance company can tell you exactly what you will get at any point in the future.

What that means is

Let’s say you are between ages 70 to 84 and you have $400,000 of qualified funds, and you are taking Required Minimum Distributions from the entire $400,000. You could transfer 25% up to $125,000 into a Qualified Longevity Annuity Contract, or in this case $100,000. After repositioning $100,000 into a QLAC, you still need to take RMD’s from $300,000 every year. However, every year you postpone making a withdrawal from your QLAC, you avoid paying taxes on that money.

The only thing worse than dying is outliving your money

With a Qualified Longevity Annuity Contract, you can ship the risk of outliving a portion of your money to an insurance company, to take advantage of their mortality credits and hedging strategy. The Insurance company provides you a promise to pay a certain amount every the rest of your life, regardless of market conditions. That payment promise could be important if your other retirement income sources have run out.

With a Qualified Longevity Annuity Contract, you can ship the risk of outliving a portion of your money to an insurance company, to take advantage of their mortality credits and hedging strategy. The Insurance company provides you a promise to pay a certain amount every the rest of your life, regardless of market conditions. That payment promise could be important if your other retirement income sources have run out.

Where can the money come from:

You can transfer the lesser of 25% of your qualified funds up to $125,000 from:

• A traditional IRA or IRA rollover (but not from a Roth or Inherited IRA).

• An employer-sponsored 401(k), 403(b) and government-sponsored 457(b) (but not from a Defined Benefit plan)

Non-qualified money from a bank CD, checking or savings account, is not allowed.

Income for one life, or two?

The only payout from a Qualified Longevity Annuity Contact is for a lifetime. That lifetime payment can be for your life, or you and another person. If you chose two lives, the payout would be less than for one life, but the payment will last until the last person dies.

The only payout from a Qualified Longevity Annuity Contact is for a lifetime. That lifetime payment can be for your life, or you and another person. If you chose two lives, the payout would be less than for one life, but the payment will last until the last person dies.

We do not recommend this

In a joint payout, you could have a payment reduction at the death of the first person. While you get more when both people are alive, a decrease in income can shortchange the survivor. Most people prefer a joint 100% payment for each person.

What do your heirs get?

If you die before starting your benefit, your beneficiaries have 100% of the premium returned to them. You can choose the cash refund rider to make sure anything left over is passed on to your beneficiaries once you begin drawing income. Or you can take a higher monthly payment and leave nothing to your heirs.

You have no fees

You have no fees

On the positive side, a Qualified Longevity Annuity Contract has no annual fees. A Longevity Annuity (QLAC) is all about income. You get an income based on the customizable income benefit you choose. There are no fees.

You have no market risk

Income from a Qualified Longevity Annuity Contract does not have any market risk. A QLAC can provide correction protection. An unfortunate sequence of returns, where you retire and lose a lot of money on Wall Street early on in retirement, could cripple your retirement plans. A steady future income may be a better choice.

What that means is:

Unlike money in the bank or on Wall Street, with a Qualified Longevity Annuity Contract, you do not need to worry about chasing x percent return that cannot be guaranteed by your banker or broker. You are guaranteed an income that will last you a lifetime. You have transferred the risk of living too long to the insurance company.

Unlike money in the bank or on Wall Street, with a Qualified Longevity Annuity Contract, you do not need to worry about chasing x percent return that cannot be guaranteed by your banker or broker. You are guaranteed an income that will last you a lifetime. You have transferred the risk of living too long to the insurance company.

Your income can increase each year

Want to fight inflation? Then purchase your Qualified Longevity Annuity Contract with a Cost Of Living Adjustment (COLA) rider. You chose the percentage increase (such as 1% to 5%), and that is the set amount your income will increase each year.

Wait up to age 85 to get your first RMD.

You can defer taking money from your Qualified Longevity Annuity Contract until age 85. Or you can start taking your lifetime income sooner. You choose the income payment date that works best for you.

Not all Longevity Annuities are a QLAC

The Deferred Income Annuity (DIA) also known as a longevity annuity, has been around since 2004. Just because you own a DIA or longevity annuity does not mean it is a Qualified Longevity Annuity Contract. You must buy it as a QLAC. A DIA does not just automatically convert to a QLAC.

Choose, but chose wisely.

When you buy a Qualified Longevity Annuity Contract, you are giving your money to a longevity insurance company who in return gives you a promise to pay you the future income you chose. You are purchasing that income with a lump sum payment. A QLAC has:

When you buy a Qualified Longevity Annuity Contract, you are giving your money to a longevity insurance company who in return gives you a promise to pay you the future income you chose. You are purchasing that income with a lump sum payment. A QLAC has:

• No cash surrender value.

• No accumulation value.

• Zero liquidity.

• No growth potential.

Why is this important?

For almost all Qualified Longevity Annuity Contracts, once you give the longevity insurance company your money to start the contract, you cannot get your money back. However, in exchange for your premium, you will know exactly what you will receive in future income.

What is the Return On Investment?

If you have a birth certificate with an expiration date on it, it is easy to figure out what your return on investment will be. Since expiration dates on birth certificates do not exist, there is no way to calculate your Return On Investment (ROI) until death. Since there is no cash surrender value in a Qualified Longevity Annuity Contract, there is no chasing x percent return that cannot be guaranteed. Therefore, there is no ROI.

If you have a birth certificate with an expiration date on it, it is easy to figure out what your return on investment will be. Since expiration dates on birth certificates do not exist, there is no way to calculate your Return On Investment (ROI) until death. Since there is no cash surrender value in a Qualified Longevity Annuity Contract, there is no chasing x percent return that cannot be guaranteed. Therefore, there is no ROI.

QLAC’s in 401k’s

401(k) plans at their option can choose to offer a Qualified Longevity Annuity Contract option to plan participants. However, with lack of demand by plan participants, only a handful of 401(k) plans are offering a QLAC.

How is my QLAC reported to the IRS?

Your insurance company sends in form 1098-Q to the IRS to report the status of your longevity annuity as a Qualified Longevity Annuity Contract (QLAC). Once you start receiving income from your QLAC, you will be sent a form 1099-R from your insurance company. The 1099-R form reports the taxable income you received from numerous sources including your QLAC.

Be Advised:

Withdrawals from a Qualified Longevity Annuity Contract before age 59½, could be subject to an additional 10% federal income tax penalty on any gain.

Avoid Banks, Brokers, and Captive Agents

Find an independent financial professional that specializes in income planning who is not tied to a bank, brokerage house or insurance company. Bankers, brokers and captive agents generally have a limited inventory of Qualified Longevity Annuity Contracts to offer. Independent financial professionals can generally offer you more choices and may be in a better position to shop the QLAC market.

Here is the real deal

Commissions on Qualified Longevity Annuity Contract are low compared to other annuities with income riders attached. Many agents, including some retirement seminar agents, are either unfamiliar with QLAC’s or don’t recommend them because of their low commissions.

Spend no more than you actually need

If you need $1,000 per month starting at a specific date in the future, buy that exact amount, not a penny more. Purchase your Qualified Longevity Annuity Contract from a highly rated longevity insurance company, maybe more than one. Be careful not to put too much into a QLAC. Let the longevity insurance company become responsible for you living too long.

We can’t Emphasize this enough

Remember that the income payments are backed by the financial strength and claims-paying ability of the longevity insurance company or companies you chose. It may be in your best interest to choose a highly rated company, or better yet, multiple companies. You can check ratings from sources like AM Best, Fitch, Moody's and Standard and Poor’s.

The Key to figuring it out is

If you are like most people, you probably need additional information to help you plan your retirement lifestyle and determine if a Qualified Longevity Annuity Contract is right for you. As a Bonus, we have created a guide to help you called “Start at the finish line”. It contains information to help you set goals and plan for the retirement lifestyle that you are looking for.

If you are like most people, you probably need additional information to help you plan your retirement lifestyle and determine if a Qualified Longevity Annuity Contract is right for you. As a Bonus, we have created a guide to help you called “Start at the finish line”. It contains information to help you set goals and plan for the retirement lifestyle that you are looking for.

Request a Quote to see actual dollar amounts:

- Based on your specific dollar amount or a lump sum payment. We would then look for the insurance company that pays you the maximum monthly income for that amount.

- Based on your desired monthly income amount. We would then look for the insurance company that provides you that income for the smallest lump sum payment.

QLAC's are designed to pay lifetime benefits from a single payment.

In Conclusion

The Qualified Longevity Annuity Contract (QLAC) can guarantee you a future retirement income that you cannot outlive. A QLAC can provide a future pension-like income, above and beyond Social Security and an employer-sponsored pension. A QLAC can help you reduces taxes by postponing taking a portion of your Required Minimum Distributions (RMD’s).

Finally

If you are at or near retirement, and you have any questions about the Qualified Longevity Annuity Contract or just need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

KEY BENEFITS

- No annual fees.

- No Required Minimum Distributions at age 70½.

- Can defer withdrawals up to age 85.

- Principle Protection and no Market Risk.

- Single and Joint lifetime income options and any remaining balance can go to heirs.

Articles