Multi-Year Guarantee Annuity (MYGA)

What is a Multi-Year Guarantee Annuities (MYGA)?

If you like bank Certificates of Deposit (CD’s), you will probably like Multi-Year Guarantee Annuities. The Multi-Year Guarantee Annuity (MYGA) is also known as a CD-Type Annuity or Fixed Rate Deferred Annuity. The Multi-Year Guarantee Annuity provides a guaranteed interest rate for a specified period of time, generally from three years to ten years.

If you like bank Certificates of Deposit (CD’s), you will probably like Multi-Year Guarantee Annuities. The Multi-Year Guarantee Annuity (MYGA) is also known as a CD-Type Annuity or Fixed Rate Deferred Annuity. The Multi-Year Guarantee Annuity provides a guaranteed interest rate for a specified period of time, generally from three years to ten years.

When should you buy a Multi-Year Guarantee Annuity?

The best use of a Multi-Year Guarantee Annuity (MYGA) is when your need for your money is greater than two years. However, if you might need your money in two years or less, it is probably in your best interest to just keep your money at the bank.

CD’s and MYGA’s are interest-bearing contracts

If you go to a bank to buy a bank Certificate of Deposit (CD), you sign an agreement with the bank to receive x amount of interest for a specific number of years on your deposit. If you go to the insurance company to buy a Multi-Year Guarantee Annuity (MYGA) you sign a contract with the insurance company to receive x amount of interest for a set period of time on your premium. The interest rate you receive each year is set by the contract.

If you go to a bank to buy a bank Certificate of Deposit (CD), you sign an agreement with the bank to receive x amount of interest for a specific number of years on your deposit. If you go to the insurance company to buy a Multi-Year Guarantee Annuity (MYGA) you sign a contract with the insurance company to receive x amount of interest for a set period of time on your premium. The interest rate you receive each year is set by the contract.

CD’s can be difficult at renewal

Once your bank CD has reached the end of the contract period, you usually have ten to fourteen (10 - 14) days to move your money out. If not, it will automatically renew for a new contract period of time the same length as the first. The interest paid will be whatever the current prevailing rates are at the time of renewal.

A MYGA can be much more user-friendly

Once your MYGA has reached the end of the contract period, you usually have thirty (30) days to move your money out. If not, it will typically automatically renew for a new contract period of the same length as the first. The interest paid could be the prevailing rate, but no less than the contractually guaranteed minimum interest rate stated in the contract.

There are no annual fees.

There are no annual fees.

There are usually no annual fees for a bank Certificate of Deposit. Also, the same is true of a Multi-Year Guarantee Annuity.

What can you take out each year?

Typically you can take out your interest only from a bank CD without a penalty for early withdrawal. Some Multi-Year Guarantee Annuities have that same interest-only limitation without a penalty for early withdrawal known as a surrender charge. Other MYGA’s will allow you to access up to ten percent (10%) of your total annuity value without a surrender charge.

What about taxes?

Your bank CD interest is taxed as ordinary income for each year you earn it, whether you take it or not. Your MYGA interest is also taxed as ordinary income, only if you withdraw it. Interest in a MYGA is tax-deferred if not removed, and will continue to compound interest until withdrawn.

Penalties for Early Withdrawals

If you cancel your bank Certificate of Deposit before the end of the term, you will likely need to pay a penalty for early withdrawal. If you cancel your MYGA before the end of the term, you will likely need to pay a penalty for early withdrawal called a surrender charge. Like most fixed annuities, Multi-Year Guarantee Annuities have a surrender charge schedule that varies by product.

MVA:

Some Multi-Year Guarantee Annuities may come with a Market Value Adjustment (MVA). An MVA may increase or decrease the amount of the withdrawal or cash surrender value of your contract depending on the change of interest rates since you purchased your annuity. Multi-Year Guarantee Annuities without an MVA are available but may pay less interest.

Choose Wisely

Your bank Certificate of Deposit is insured by the Federal Deposit Insurance Corporation (FDIC). Your annuity is backed by the full faith and credit of the insurance company you chose. So it can be a good idea to buy from a well-rated insurance company or companies.

Your bank Certificate of Deposit is insured by the Federal Deposit Insurance Corporation (FDIC). Your annuity is backed by the full faith and credit of the insurance company you chose. So it can be a good idea to buy from a well-rated insurance company or companies.

But with that said…..

Often the best rates are paid by lower rated companies. You still might want to buy a Multi-Year Guarantee Annuity from a lower rated insurance company. If you do, avoid giving a lower rated insurance company 100% of your available money, and you might want to limit your premium to a hundred thousand dollars ($100,000) or less.

No Conversion Options

There is no option to convert your bank Certificate of Deposit into a guaranteed lifetime income. If you annuitize your MYGA to an income annuity, you are turning your cash value into a series of income payment, possibly for life. You should check with your insurance company about the payout options.

No lifetime Income rider is available on a MYGA

The income rider option on a Traditional Fixed Deferred Annuity is not available on a MYGA. If you want a reliable lifetime income payment, you will need to annuitize your contract. When changing your annuity from a MYGA annuity into an income payment by annuitizing it, you give the cash value to the insurance company. Once you do this, it is like buying a Single Premium Immediate Annuity (SPIA), you cannot get your money back.

AVOID PROBATE

If you pass away, your money In a Multi-Year Guarantee Annuity goes to your named beneficiary(s) without passing through probate court. Most MYGA’s waive the surrender charge, if any, and give the full account value to your recipients.

Be advised:

Withdrawals may be subject to ordinary income taxes. If you are under age 59½, you could be subject to an additional 10% federal early withdrawal income tax penalty on any gain.

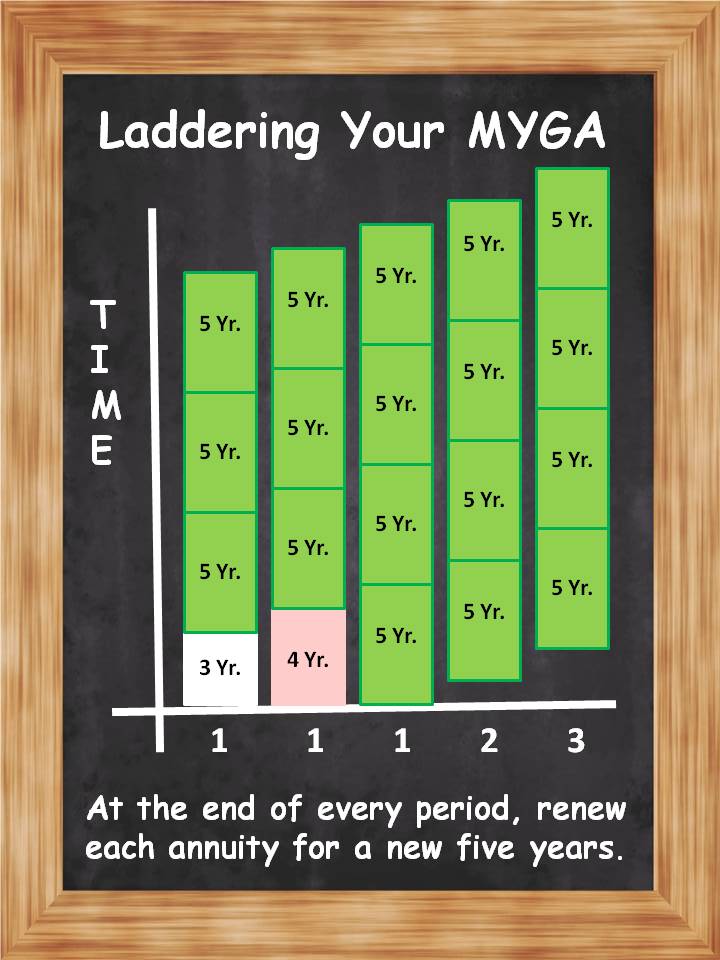

Laddering your Multi-Year Guarantee Annuity

If you have adequate income to live on today but are concerned about future income, you might consider a Deferred Income Annuity ladder. When using the laddering strategy, you split a payment into more than one annuity with different maturity dates.

Let’s assume for example you have $300,000 available to work with, in your bank account. Your ladder could look like this:

- Today buy three $60,000 Multi-Year Guarantee Annuities, one for three (3) years, One for four(4) years and one for five (5) years.

- Twelve (12) months later: Buy one (1) $60,000 five-year Multi-Year Guarantee Annuity.

- Twenty-Four (24) months later: Buy one (1) $60,000 five-year Multi-Year Guarantee Annuity.

- Thirty-Six months (3 years) later: Renew the maturing three-year Multi-Year Guarantee Annuity to a five-year.

- Forty-Eight months (4 years) later: Renew the maturing four-year Multi-Year Guarantee Annuity to a five-year.

- You now have Five (5) five-year Multi-Year Guarantee Annuities. Renew each maturing five-year Multi-Year Guarantee Annuity to a new five years.

A.K.A.

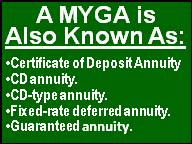

The Multi-Year Guarantee Annuity is Also Known As a:

The Multi-Year Guarantee Annuity is Also Known As a:

• Certificate of Deposit annuity.

• CD annuity.

• CD-type annuity.

• Fixed-rate deferred annuity.

• Guaranteed annuity.

In Conclusion

A Multi-year Guarantee Annuity (MYGA) provides principal protected growth. The interest rate paid is guaranteed by contract for the period of time you chose, usually, form three (3) to ten (10) years. The MYGA is a great alternative to a bank Certificate of Deposit (CD) which is why the MYGA is sometimes referred to as a CD annuity or a CD-type annuity.

Finally

If you are at or near retirement, and you have any questions about Multi-Year Guarantee Annuities or just need a little guidance, feel free to contact us. We know retirement planning can be confusing, so it is important to get the facts before you make any long-term decision.

KEY BENEFITS

- No annual fee.

- Interest rate guaranteed for a specified period of time.

- Tax-deferred accumulation.

- Principle protection.

Articles